The .Plan seems to firmly believe the S&P is off their rocker:

Marron takes a more neutral approach, pointing out that three other ratings agencies -- two in the US, one abroad -- had downgraded US credit-worthiness prior to S&P. He earlier pointed out that, technically, the US has defaulted once in 1979, because the "Treasury's back office was on the fritz". Everyone got their money back, but the result still wasn't pretty.

Addiionally, it pays to remember that S&P's rating are only about the risk of a default occuring, not the size of the default, its duration, or how much investors will eventually get back. Moody's, by contrast, includes these factors. So the fact that US bond investors are likely to get everything back, even if payment were delayed by a few days in event of a default, makes US bonds still the "assets of choice for global investors seeking a 'safe haven'"

But then, Sumner says the reactions in the relevant market (US Treasuries, not stocks) are actually against what S&P said anyway: The markets this morning gave a massive vote of no confidence to S&P ratings service, as yields plunged on Treasuries.

Very large comic below the fold

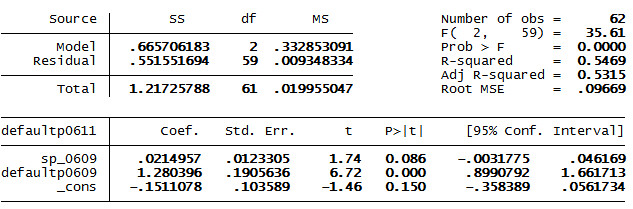

1) In fact, the evidence from the past five years suggests that it may be worthwhile to adopt a contrarian investing strategy that specifically bets against S.&P.’s ratings. ...

{kind=link}

2) Back when I was an in-house lawyer for an investment bank, I had extensive interactions with all three rating agencies. We needed to get a lot of deals rated, and I was almost always involved in that process in the deals I worked on. To say that S&P analysts aren’t the sharpest tools in the drawer is a massive understatement.Boudreaux is confused:

Why is the first remotely serious effort in ages to oblige government not to borrow beyond a certain limit portrayed as fiscal imprudence?But perhaps that is because he is making the mistake of taking what politicians say at face value. There was never a danger of them not raising the debt ceiling. The brinksmanship was theater. The points S&P make are that 1) politics should be about more than theater, and 2) even with this disfunctional yelling match, so little of the deficit was actually addressed. Now, a 5% reduction in the deficit over 10 years is nothing to sneeze at. It's a start. But there doesn't seem to be much willingness for either side to address their sacred cows, and until they do the outlook is for more deficits as far as the eye can see ... and that sounds more like imprudence than prudence. On the other hand, I'm not entirely certain that the theater is a significant change from the status quo over the last 20 some-odd years.

Marron takes a more neutral approach, pointing out that three other ratings agencies -- two in the US, one abroad -- had downgraded US credit-worthiness prior to S&P. He earlier pointed out that, technically, the US has defaulted once in 1979, because the "Treasury's back office was on the fritz". Everyone got their money back, but the result still wasn't pretty.

Addiionally, it pays to remember that S&P's rating are only about the risk of a default occuring, not the size of the default, its duration, or how much investors will eventually get back. Moody's, by contrast, includes these factors. So the fact that US bond investors are likely to get everything back, even if payment were delayed by a few days in event of a default, makes US bonds still the "assets of choice for global investors seeking a 'safe haven'"

But then, Sumner says the reactions in the relevant market (US Treasuries, not stocks) are actually against what S&P said anyway: The markets this morning gave a massive vote of no confidence to S&P ratings service, as yields plunged on Treasuries.

Very large comic below the fold

No comments:

Post a Comment